U.S. Lending Crisis: Has Student Debt Threatened American Dreams of Home Ownership?

For many recent graduates, the American Dream of home ownership has become a distant concept which may be unattainable in practical terms. Rising tuition costs in the United States have fueled a trillion-dollar crisis in student debt that is preventing more and more people from buying a car or securing a mortgage on a home. These troubling trends show that the use of budget tracking tools may be more important than ever, so that consumers can monitor spending habits in more efficient ways and keep debt payment schedules manageable.

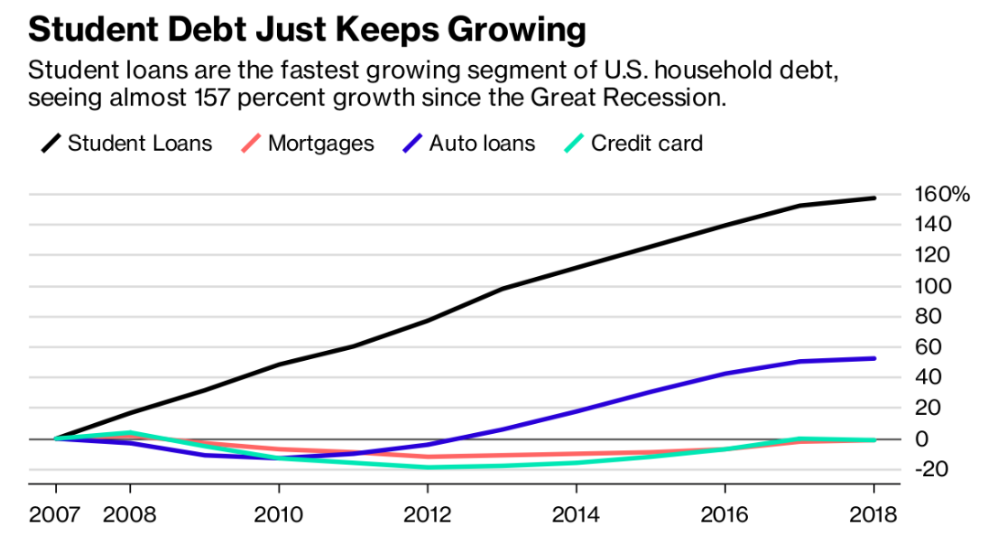

(Source: Federal Reserve Economic Data)

Recent reports on the economy show new records, as nearly two-thirds of all college graduates fishish school with debt. In the United States, a national epidemic as emerged with roughly nine million people defaulting on their loan agreements and outstanding student debt reaching staggaring total of $1.5 trillion. Student loans can prevent credit applications from being approved, and these trends continue to negatively influence the financial well-being of roughly 44 million Americans.

Student Debt as ‘National Crisis’

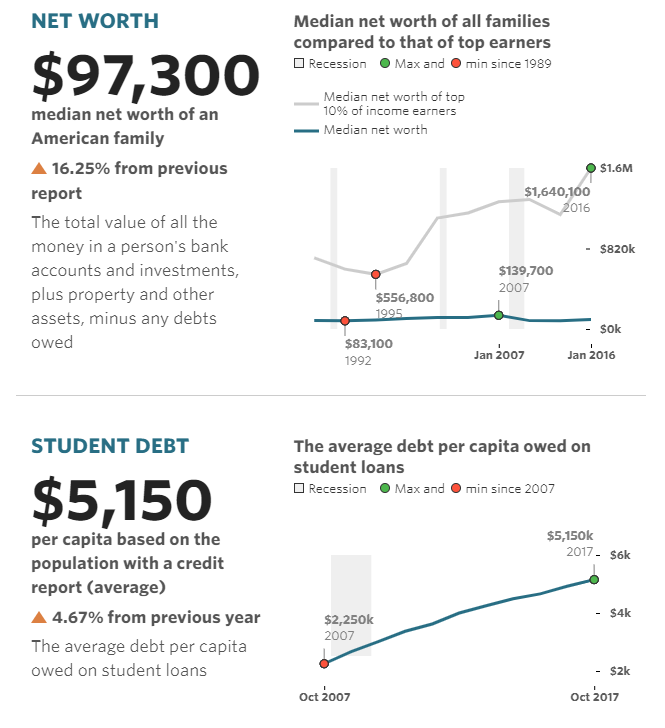

Home ownership is often a future indicator of net worth, civic participation, long-term educational attainment, overall physical health, and general quality of life. But the average student now graduates with more than $40,000 in debt related to the costs of education. This indicates a substantial increase of roughly $23,000 relative to the government data statistics from 2001. Elevated monthly repayment obligations that accumulate as a result of these upward trends can create critical financial problems for new graduates, as this is money which could otherwise be used to start a business, buy a car, or initiate the down payment that is typically required to buy a new home.

Last November, U.S. Secretary of Education Betsy DeVos described the trend in student loan debt as a ‘national crisis’ and this assertion seems to be supported by the official data projections. In 2019, student loan debt is expected to surpass auto loans and credit cards as the second-largest category of consumer debt (falling behind only U.S. mortgage loans in aggregate). By 2023, it is estimated that 40% of all student loan borrowers may be at risk of default on these obligations and this is an event which can have a dramatic impact on long-term credit scores for nearly every age demographic.

(Source: U.S. Census Bureau)

Unfortunately, these statistics are not simply academic or abstract concepts. These trends are influencing the lives of real people and they are preventing younger generations from achieving their home ownership goals. This is why it is important for young adults to use budgeting strategies which properly structure debt-to-income relationships. Using these strategies, consumers can limit the negative consequences of compounding debt interest over time.

(Source: Bank of America)

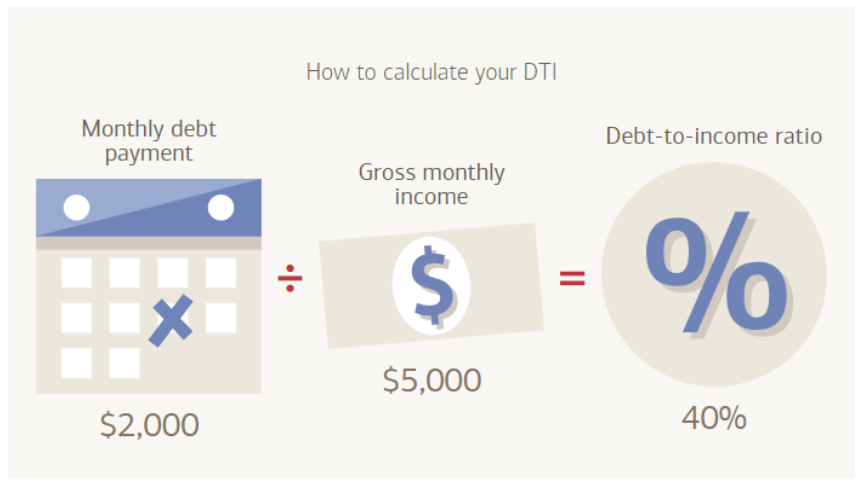

When looking for help in managing your money, it is critical to use budget tracking tools to monitor spending habits in a more objective way. Moreover, the following strategies can put consumers with student debt in a better position to maximize application approval from home lenders:

- Lower your debt-to-income ratio (DTI) percentages by as much as possible

- Refinance student loans to reduce interest rates and lower monthly payments

- Pay all student loans on time (and never miss the payment schedules)

As is the case with most issues in personal finance, early planning efforts tend to work best in preventing budgeting mistakes in the future. Of course, this is often easier said than done. But with the right level of financial discipline consumers can work to mitigate the downside effects of our national student loan epidemic. If home lenders see a solid history of on-time payments and reasonable levels in the DTI ratio, it is often much easier to achieve loan approval and get started on the path back toward the American Dream of home ownership.